Brazil is the epicenter of the Latin American fintech boom, but entering this market is not an exercise in regulatory arbitrage. The Banco Central do Brasil (BCB) and the financial intelligence unit, COAF (Council for Financial Activities Control), operate one of the most technologically advanced and heavily monitored financial infrastructures globally.

If your neo-bank attempts to launch in Brazil using a generic, "off-the-shelf" global compliance template, you will face catastrophic failure. Under regulations like BCB Circular 3.978, digital institutions are held strictly liable for the identities of the users on their ledgers.

For CTOs and Heads of Expansion, the challenge is a brutal balancing act: you must build an onboarding architecture capable of stopping sophisticated synthetic identity rings and PIX fraud, without introducing onboarding friction that spikes your Customer Acquisition Cost (CAC) and kills conversion rates.

The PIX Paradox: Hyper-Growth vs. "Contas Laranja"

You cannot operate a neo-bank in Brazil without natively integrating PIX. It drives the entire digital economy. However, PIX’s real-time settlement speed is its greatest vulnerability, giving rise to the primary existential threat for Brazilian neo-banks: Contas Laranja (Orange Accounts / Money Mules).

Fraudsters systematically target newly launched neo-banks with weak KYC pipelines. They use stolen or rented IDs to open thousands of accounts. When these criminals commit fraud elsewhere, they use PIX to instantly funnel the stolen funds into these "orange accounts" on your platform, immediately cashing out to crypto exchanges.

COAF tracks this telemetry relentlessly. Through mechanisms like the MED (Mecanismo Especial de Devolução), the central bank forces institutions to return fraudulently acquired PIX funds. If your neo-bank is identified as a safe haven for contas laranja, the BCB will freeze your operations and mandate crippling capital reserve requirements.

Architecting a Compliant Brazilian Onboarding Pipeline

Your KYC API cannot be a passive data collection tool. It must act as a synchronous gatekeeper designed to break synthetic identity attacks at registration, while processing legitimate users in under 3 seconds to prevent drop-off.

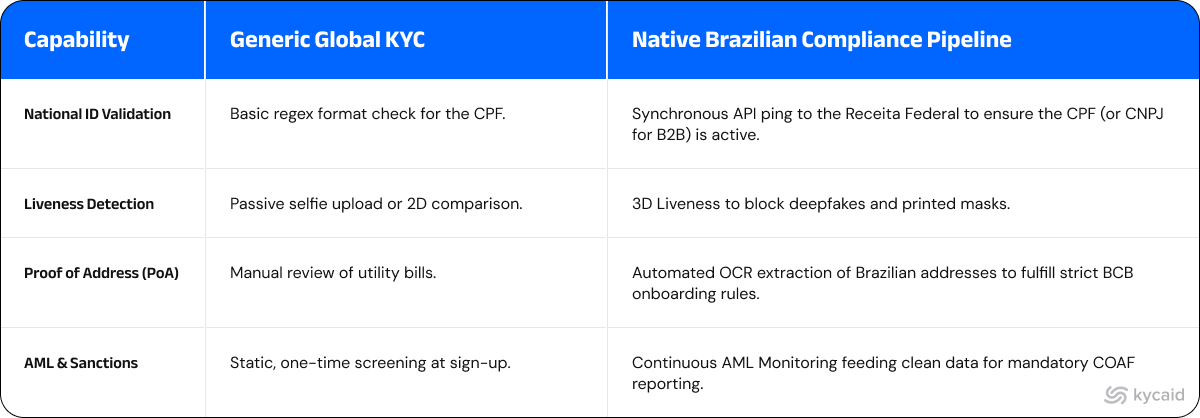

Generic KYC vs. Native Brazilian Identity Pipeline

A standard document check is mathematically insufficient. Fraud rings possess high-quality physical forgeries of RGs (Registro Geral) and CNHs (Driver’s Licenses). Your backend architecture must execute a synchronous cross-reference between the physical document, the user's live biometrics, and federal databases.

The KYCAID Solution: Native Brazilian Identity Infrastructure

KYCAID provides the exact architectural primitives neo-banks need to scale safely in Latin America. We replace fragmented local vendors with a single, unified API engineered for the complexities of the Brazilian market.

When a user attempts to open an account, KYCAID executes the entire identity workflow in under 3 seconds to preserve your CAC metrics:

- ➀ Data Capture & Biometrics: The user scans their RG/CNH and performs an iBeta L2 certified liveness check.

- ➁ Synchronous Federal Ping: Our API validates the CPF (for retail) or CNPJ (for business accounts) directly against the Receita Federal to ensure the status is "Regular".

- ➂ PoA & AML Screening: We extract the Proof of Address via OCR and run the user against global PEP and Sanctions lists.

- ➃ Webhook Execution: We return a definitive JSON payload to your backend, enabling your FinOps team to programmatically approve legitimate users and permanently block synthetic identities.

Your neo-bank achieves hyper-growth, your conversion rates remain intact, and your MLRO has the immutable audit logs required for COAF compliance.

Stop compromising your LatAm expansion with generic compliance tools.

FAQ: Neo-Bank Compliance in Brazil

What are "Contas Laranja" (Orange Accounts) in Brazil?

"Contas Laranja" are money mule accounts created using stolen, rented, or synthetic identities. Criminals use these accounts within neo-banks to receive and launder illicit funds via PIX before cashing out, transferring the regulatory liability onto the neo-bank.

Why is CPF/CNPJ validation critical for Brazilian Neo-banks?

The CPF (individual) and CNPJ (business) are the anchors of Brazilian identity. The BCB requires synchronous validation against the Receita Federal database to ensure the ID exists, is legally active, and mathematically matches the user opening the account.

What is the role of COAF and BCB Circular 3.978?

BCB Circular 3.978 mandates strict Anti-Money Laundering (AML) protocols. Institutions must implement robust, risk-based identity verification (including Proof of Address and Continuous Monitoring) and report suspicious activities to COAF, Brazil's financial intelligence unit.